With so much disruption on the UK’s political landscape it may be difficult to see the wood for the trees. Tucked away in the Autumn 2018 budget was a valuable temporary tax relief which has gone largely unnoticed but which could allow businesses to invest and grow – effectively benefitting from £1 tax relief for every £1 spent on plant and machinery purchases.

The Annual Investment Allowance (AIA) relief allows expenditure on plant and machinery purchases up to the AIA limit to be set against company profits in the year the expenditure occurs.

In 2018 the AIA stood at £200,000 and rose to the new threshold of £1m from January 1st 2019 for two years, making it a valuable incentive for large-scale investment for growth or replacement of ageing equipment and machinery.

But with a deadline of January 1st 2021 when the allowance reverts back to its former £200,000, it is essential that any company embarking on significant capital expenditure begins consulting with their accountant now to maximise on any available tax relief. Poor planning and timing could mean missing out on the available tax relief, or even worse, paying more tax than is required.

By increasing the relief on qualifying expenditure up to a £1,000,000 limit, those businesses already spending up to the £200,000 threshold have a considerable incentive to increase or bring forward their capital expenditure on plant and machinery.

JCB Finance managing director Paul Jennings, said: “This important tax incentive allows 100% tax relief in the first year and is designed to encourage businesses to invest in plant, machinery, commercial vehicles and a broad range of other assets.

JCB Finance managing director Paul Jennings, said: “This important tax incentive allows 100% tax relief in the first year and is designed to encourage businesses to invest in plant, machinery, commercial vehicles and a broad range of other assets.

“Depending on the business’ rate of tax, it is an open invitation to invest in plant and machinery and secure the equivalent of a 19% to 45% subsidy. Better still – if you acquire the plant via a Hire Purchase agreement the acquisition, for tax purposes, is treated as if cash had been paid. Plus any interest payable is tax deductible too.

“However, different financial year ends will affect the proportion and timing of expenditure. Getting the timing and the amounts right is crucial to your business. We are already recommending to our customers that they speak to their accountant and to our JCB Finance team now, so they can plan the optimum time to take delivery of their machinery.”

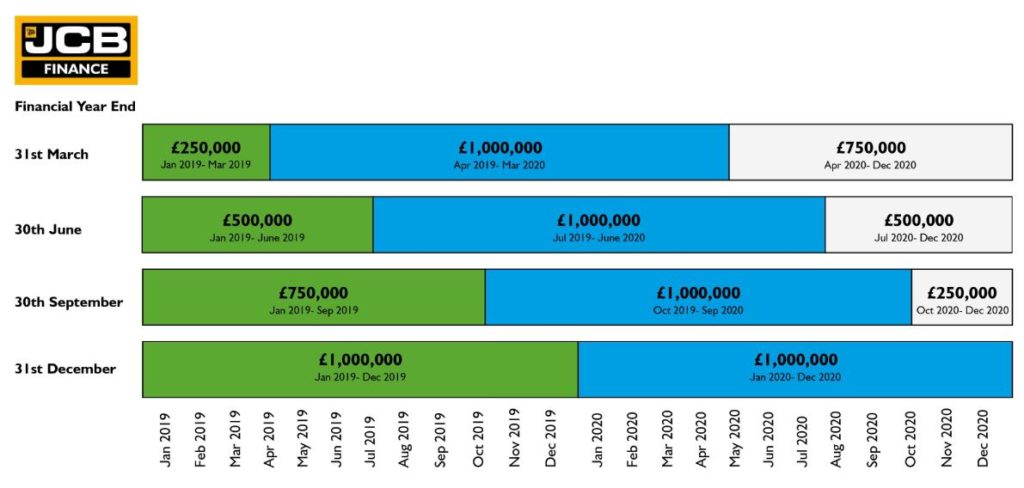

The chart below illustrates the maximum amounts available by showing four different company financial year ends, and how vital it is to spend the right amount within the right periods in order to maximise tax benefits. Different financial years that straddle either the tax year or calendar year may result in complicated calculations that could lead to a lesser AIA being granted in that financial year. Given the lead times of some plant and machinery from order to delivery, this also needs to be carefully factored in to buying plans.

JCB Finance have been providing asset finance and supporting business growth in the construction, agriculture and industrial sectors since 1970, so understand the challenges these customers may face. Their team can offer fast, flexible finance solutions that help businesses preserve their working capital by spreading the cost in a tax efficient manner.

Finance options are not restricted to JCB plant and machinery equipment, but are also available for other non-competitive new machinery, cars, commercial vehicles and used plant.